The Anatomy of Logistics in India

Startups and **** Series

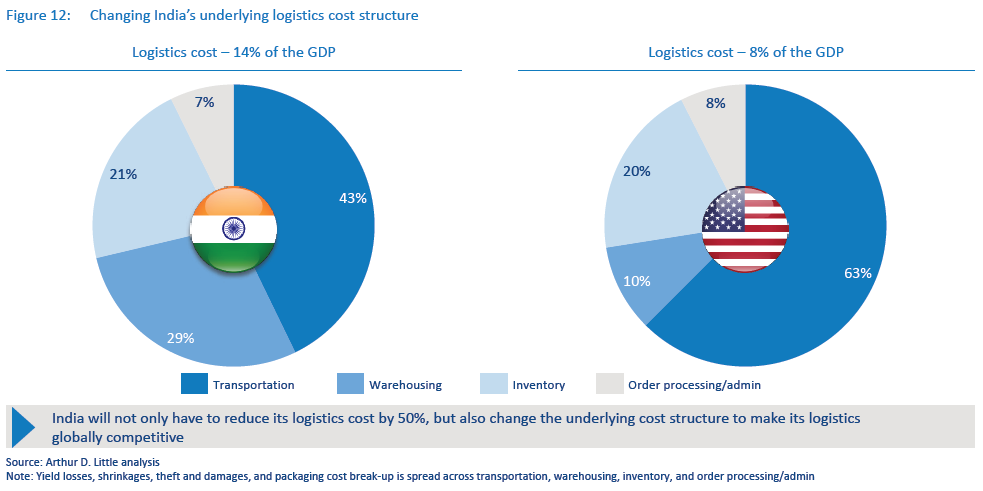

The pandemic has been tough for all of us disrupting lives, supply chains and industries alike, these unprecedented times though have proved to be the inflection point for the logistics sector. With the world largely being closed and people moving online for almost every need, the onus fell on the sector to ensure the global flow of goods, particularly the essentials. Considered as a supporting sector for long it has now transformed into an essential one. Indian logistics spend stands at 14% of the country’s GDP against a global average of 8%, to address this the government is set to announce a National logistics policy to put it at par with global standards. According to the World Bank Logistics Performance Index, India will be one of the top 20 countries by 2030. The supply chain industry is to be optimized and an automated logistics ecosystem, with a simplified distribution system powered by next-gen technologies such as big data, AI, blockchain, and the Internet of Things will be the way forward. In this piece, I will go a little deeper and give you a quick report of the sector, the market and the trends.

Market and Background

The Indian logistics sector is valued at USD$ 215 Bn, contributing 14% of the country's GDP and is expected to grow at a CAGR of 10.5% over the next 4 years. The pandemic has been a boon for the sector, once considered as a supporting service sector it has transformed into an essential and mainline sector. A national logistics policy is set to be announced this year which may further boost the industry.

The industry was fragmented and often subject to delays and unreliability. E-commerce was the first market force that brought speed and fulfilment to the forefront as it would be very difficult to retain customer trust otherwise. The next market force was GST, earlier the industry was operating around the premise of minimizing taxes. The warehousing, fulfilment and operations were a function of tax rather than speed, this changed after GST and there has been efficient optimization for speed ever since.

The Indian logistics industry is associated with high cost of transportation and storage. A significant proportion of the higher cost can be attributed to the absence of efficient intermodal and multimodal transport systems, poor road infrastructure leading to lowering the maximum distance covered by any commercial vehicle and toll on the highways. Further, higher warehousing costs are driven by a shortage of warehousing capacity in India, non-standardization of warehouses in terms of IT application among other reasons. A report by JLL states that 80% of the logistic cost can be optimised through an efficient mode of transportation, just in time inventory management, efficient and time-saving handling system, where location and scale of warehouse is the vital factor.

The pandemic has brought the industry to light with the capital flow towards it increasing, we can expect to see many disruptions in the space. Last year alone 452 Mn was pumped across 40 deals towards startups working in the sector.

Key Trends

Sectors like e-commerce and third-party logistics will drive the demand for warehousing followed by pharma, engineering and manufacturing.

The demand for warehousing is expected to grow around 160% to reach 35 million sq ft in 2021

The ever increasing demand from the time-sensitive e-commerce sector has changed the dynamics of the logistics industry. Businesses are now on the lookout for logistics service providers who are capable of integrating more technology, process and automation helping them to move closer to their end consumers.

COVID-19 has also exposed the challenges of consolidation within the warehousing sector. Going forward, the market is expected to decentralise to mitigate future disruption, ensure business continuity, and ease operations. The rise in online businesses may eventually lead to a surge in new warehousing demand along with a rising trend of multi-level warehouses within the city limits

Last-mile delivery is the biggest challenge. With all sellers going online in one way or the other. Robotics and technology such as drones are set to occupy the space in the future of the logistics arena in offering new-age solutions driving cost reduction, convenience, and delivery cycle.

A National Logistics policy that would provide an agile regulatory environment through a unified legal framework for the “One Nation-One Contract” paradigm has been framed and is set to roll out soon.

Increase in the adoption of multi-modal services. The pandemic has shown the need to leverage both rail & road a lot more effectively rather than viewing them as separate modes of transportation. Companies have realized the need for real-time visibility and first-last mile delivery to support large scale operations with maximum efficiency for which Infrastructure development, accelerated regulatory support and a technology ecosystem is required.

Future Trends

The growth is going to come from Tier2 and Tier 3 cities

Due to the nationwide lockdown, the restricted movement has underscored the importance of in-city warehousing, with tier II and III locations emerging as preferred investment destinations, due to policy initiatives like GST, assigning infrastructure status.

The Government of India’s focus on making India a global manufacturing hub has caused warehousing clusters to expand rapidly beyond the top cities to tier-2 and 3 cities. Also, as most of the tier-2 and 3 cities in India are aligned with industrial hubs the demand for Grade-A warehouses in these cities has increased substantially. The increasing internet penetration in rural areas, in addition to rising household income and the government’s push on digitizing rural areas, has increased the pressure on companies to move closer to their customer base in these areas. In the process to cater to the hugely untapped rural customer base, organisations have realised the importance of developing quality warehousing facilities that not only offer operational excellence but also facilitate cost optimisation.

Over the last two to three years, there have been a number of third party logistics providers that have come up, taking care of the last-mile delivery for e-commerce companies in Tier 2 and 3. We will see logistics value chains in terms of storage and hyperlocal deliveries grow significantly in tier 2,3.

Development of the infrastructure facilities like dedicated freight corridors, free trade warehousing zones, logistics parks and container freight stations are expected to improve the efficiency of the Indian logistics market.

The focus will be on technologies such as Robotic process automation (RPA), real-time data analysis, IoT (to ensure smooth, efficient, and transparent operations), AI (to be integrated as a tech-enabler in tackling demand and to proactively deal with fluctuating demands across supply chain operations), Blockchain (to adopt more blockchain-based documentation to get rid of unnecessary printing, scanning, and emailing).

Expectations: Maximising the use of existing infrastructure, Adoption of Tech for fleet management, quick decision making and route optimization, Agile Supply chains (responsive supply chain - a combination of speed, cost, and efficiency).

Government policies: Commitment to modernizing the functionalities of Indian logistics with a key concentration on infrastructure development, Goods and Services Tax, (GST), relaxed FDI regulations and granting of infra status to boost the core competencies of the Indian logistics industry. Sagarmala is a determined national initiative aimed at bringing change in India’s logistics performance by cracking the full potential of India’s coastline and waterways. Atmanirbhar Bharat Abhiyan package, which included measures towards improving the state of the warehouses in the Agri-space are few favourable policies and a holistic national logistics policy is expected to roll out soon to further facilitate the sector.

Conclusion

I believe the industry is at an inflection point with business going online Third-party logistics, Adoption of technology and efficient management systems will be the key driving factors for the industry going forward. A lot is also expected from the National logistics policies, the policies towards the sector so far have been favourable and the right framework can help accelerate the growth. I have been seeing a growth in the number of startups trying to disrupt the industry, The startup ecosystem has moved beyond internet business today we have founders focusing on problems across industries and logistics has its misfits, Last year itself $432 mn was pumped into startups working in the sector to accelerate the innovation, I am very excited to see how things turn out. Our startup ecosystem has matured and today there is no constraint for capital to start and grow a business, If there ever was a perfect time to start up this is it.

Sources: Adlittle, JLL, economic times, yourstory, cargotalk, mordorintelligence, financial express, business wire, kpmg.