The Anatomy of Rupeek

Startups and **** Series

We as a country have an emotional affinity to gold, Gold and its purchase is deeply embedded in our culture and gold is also the primary asset many poses. The World Gold Council estimates that Indian households are sitting on a $1.5 trillion hoard of gold. Due to this emotional affinity, gold is usually mortgaged than sold, Gold loans are one of the oldest forms of credit and have been dominated by local moneylenders and pawnbrokers, even today they occupy 65% of the market so there is still a lot of room for organized players to gain market share. Organized players like Gold NBFCs (Muthoot, Mannapuram), one of the most profitable lenders in the country have built a strong network and continue to increase their presence, however these existing players both organized and unorganized charge interest rates as high as 50% and are not very customer friendly. The biggest threat to the NBFC giants are VC backed startups like Rupeek, Rupeek is the country's fastest-growing tech startup, the online gold lender has registered a staggering 3-year revenue growth of 7,295%. In this article I will dive a little deeper into the market and try to put together a case for rupeek and why I think startups can beat the established players.

Overview

Rupeek is a financial services company that operates an online lending platform to give gold loans at the doorstep of the customer, its mission is to bring financial inclusion for the masses and introduce products that are transparent and people-friendly. Rupeek primarily caters to the Tier 1,2 markets and is beginning to capture the market quickly with presence in 27 cities.

Market and Background

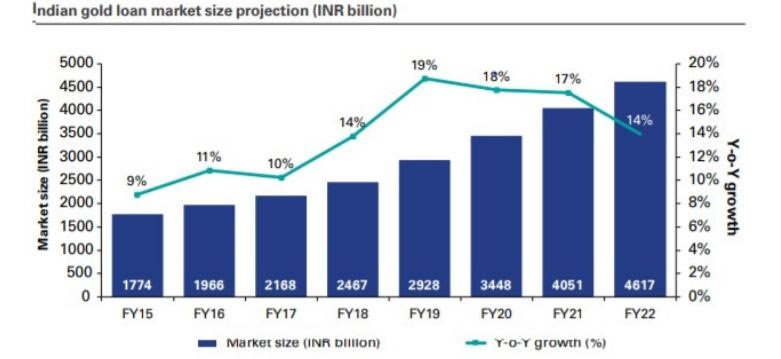

Indian Gold Loan market is valued at INR 4051 Billon and is expected to grow at a compounded annual growth rate of 15,7%, post-pandemic there is a surge in gold loans due to the economic downturn, many SMBs have also been looking at gold loans to help them steer pass the uncertainties.

Gold loans have high LTV(loan to value - up to 90%), They are multipurpose, there are no restrictions on the usage of loans. Minimal KYC is required, Turn around time is minimal. They accommodate small ticket loans of value as low as Rs 3000/- and there is the convenience of repayment. These factors make gold loans attractive, especially in areas where gold is usually the primary asset class and people are not used to the heavy documentation a bank loan would require.

In recent years, gold loans have become popular in urban areas as well. A key reason for this is that gold loan rates compare favourably with those available on personal loans. With frequent hikes in interest rates by the RBI and the subsequent hike in rates by banks, the cost of personal loan borrowing is increasing. This has led to an increased consumer willingness to secure gold loans. The taboo of using gold as collateral is also drifting away.

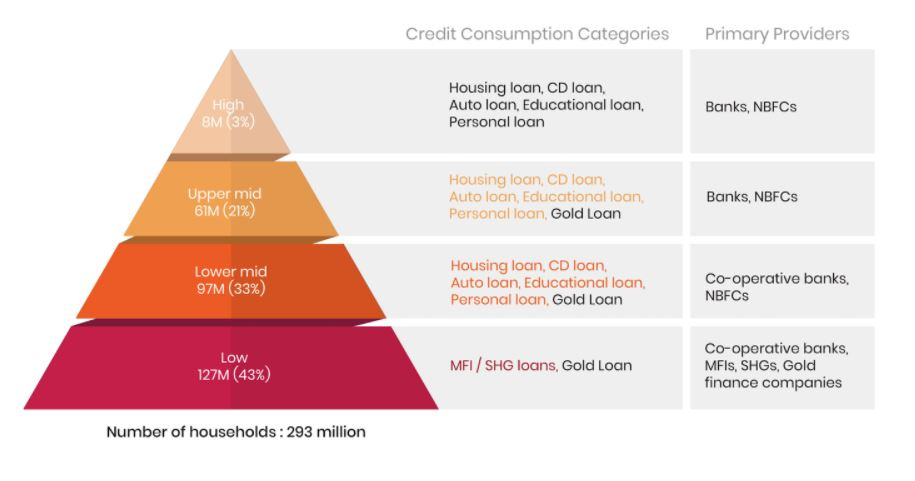

The unorganized sector (Moneylenders/pawnbrokers) commands 65% of India’s gold loan market The local money lenders have higher market penetration and advantage of minimal or no documentation and a higher Loan to Value (LTV) ratio than organised players. The rest is dominated by gold NBFCs like Muthoot, Malappuram. Interest rates of unorganized > Interest rates of NBFCs > Interest rates if banks.

Banks despite low-interest rates lack the focus, Gold loan is a specialized business, it is operationally extensive, Gold Loan is primarily small ticket in nature (~Rs 60k) and has a tenure of only around 4 months. building a small 1000 cr gold loan AUM requires an organizational infrastructure that can deal with lakhs of borrowers every month. In comparison, building a 1000 cr mortgage book requires dealing with less than 100 borrowers a month. NBFCs on the other hand also have a competitive advantage as they require minimal documentation and have a turnaround time of around 15minutes.

So, how do we get the banks into the picture? Well, that's where rupeek comes in!

Journey and Strategy

While running his family business Sumit, the founder of rupeek applied for a loan at a large NBFC which was rejected by the lender, this left Sumit in shock as he failed to get a loan despite having run a successful business of over 10 years, this led to the realization about how hard it must be for others in the ecosystem to get access to credit. This realization led to the founding rupeek to provide convenient and cost-efficient credit to the Indian consumers. Today, Rupeek is India’s fastest-growing asset-backed digital lending platform enabled by technology and an automated asset-light supply chain, Rupeek is giving the centuries-old business a much-needed technology makeover.

Rupeek offers gold loans at the customer’s doorstep and completes the loan underwriting-to-disbursal process within 30 minutes. By cutting down on expenses with an online-only strategy. While Rupeek has a non-banking financial company (NBFC) licence, it primarily lends through its banking partners and not from its own book and has around 15 major banks onboard as lenders across various levels of integration with Rupeek.

This bank tie-up helps rupeek to offer lower interest rates, keep it operationally nimble, while also cashing on the point that it uses the bank's secure locker infrastructure for storage. The tie-up also helps rupeek expand quickly. This on the other hand helps banks to cash in on the gold loan market with rupeek doing the heavy lifting. It's a win-win.

“Gold-backed lending currently faces several challenges in the country - high-interest rates, social stigma and friction. None of the existing players have solved all these challenges. Gold loans are a perfect tool to monetise idle gold assets in the country and our offerings solve all the

gold-backed lending challenges. We are building a differentiated business model from the ground up, powered by state-of-the-art technology and an automated, asset-light supply chain.” - Sumit Maniyar, founder Rupeek.

Business Analysis

Rupeeks model is fairly simple, other lending categories require extensive underwriting capabilities to understand borrower cash flows, intent to repay, quality of the collateral, etc Whereas a gold loan transaction is straightforward because gold is a secured asset and there is no requirement of any other collateral.

Rupeek charges an interest rate of 9-10% an annum which is significantly less than any other competitor, as rupeek lends from the books of a banking partner it takes commission on the transaction from the bank.

The sequoia backed startup has so far raised $138.5 mn over 6 rounds from marquee investors and is scaling aggressively. It is a potential unicorn.

Conclusion

Gold loan is a huge market in India and there is massive untapped potential, it will be important for rupeek to gain customer trust and overcome the social stigma associated with the pledging of gold to grow multifold going forward.